|

Audit and Risk Committee Komiti Taiwhenua

AR20-1 Thursday, 27 February 2020 Council Chambers Barkes Corner, Tauranga 1.00pm

|

|

Audit and Risk Committee Komiti Taiwhenua

AR20-1 Thursday, 27 February 2020 Council Chambers Barkes Corner, Tauranga 1.00pm

|

|

27 February 2020 |

Audit and Risk Committee

Membership

|

Chairperson |

Mayor Garry Webber |

|

Deputy Chairperson |

Cr James Denyer |

|

Members |

Cr Grant Dally Cr Mark Dean Cr Murray Grainger Cr Anne Henry Cr Christina Humphreys Cr Monique Lints Cr Kevin Marsh Cr Margaret Murray-Benge Cr John Scrimgeour Cr Don Thwaites |

|

Quorum |

6 |

|

Frequency |

Quarterly |

Role

To provide assurance and assistance to the Western Bay of Plenty District Council on management of Council's risk, financial control and compliance framework, and its external accountability responsibilities.

Scope

· Recommend to Council an appropriate risk management strategy and monitor the effectiveness of that strategy.

· Monitor the Council’s external and internal audit process and the resolution of any issues that are raised.

· Review key formal external accountability documents such as the Annual Report in order to provide advice and recommendation in respect to the integrity and appropriateness of the documents and the disclosures made.

· Provide a forum for communication between management, internal and external auditors and the governance level of Council.

· Ensure the independence and effectiveness of Council’s internal audit processes

· Oversee the development of the council’s Annual Report.

· Oversee the development of financial policies.

· Monitor existing corporate policies and recommend new corporate policies to prohibit unethical, questionable or illegal activities.

· Support measures to improve management performance and internal controls.

Responsibilities:

External Audit and External Accountability

· Engage with Council’s external auditors regarding the external audit work programme and agree the terms and arrangements of the external audit in relation to the Annual Report.

· To recommend the adoption of the Annual Report and the approval of the Summary Annual Report to Council.

· Review of the effectiveness of the annual audit.

· Monitor management response to audit reports and the extent to which external audit recommendations concerning internal accounting controls and other matters are implemented.

Internal Audit

· In conjunction with the Chief Executive and the Group Manager Finance and Technology Services, agree the scope of any annual internal audit work programme and assess whether resources available to Internal Audit are adequate to implement the programme.

· Monitor the delivery of any internal audit work programme.

· Assess whether any significant recommendations of any internal audit work programme have been properly implemented by management. Any reservations the Internal Auditor may have about control risk, accounting and disclosure practices should be discussed by the Committee.

Risk Management

· Review the risk management framework, and associated procedures to ensure they are current, comprehensive and appropriate for effective identification and management of Council’s financial and business risks, including fraud.

· Review the effect of Council’s risk management framework on its control environment and insurance arrangements.

· Review whether a sound and effective approach has been followed in establishing Council's business continuity planning arrangements.

· Review Council's fraud policy to determine that Council has appropriate processes and systems in place to capture and effectively investigate fraud-related information.

Other Matters

· Review the effectiveness of the control environment established by management including computerised information systems controls and security. This also includes a reviewing/monitoring role for relevant policies, processes and procedures.

· Review the effectiveness of the system for monitoring Council's financial compliance with relevant laws, regulations and associated government policies

· Engage with internal and external auditors on any specific one-off audit assignments.

· Consider financial matters referred to the committee by the Chief Executive, Council or other Council committees.

Power to Act:

The Committee is delegated the authority to:

· Receive and consider external and internal audit reports.

· Receive and consider staff reports on audit, internal control and risk management related matters.

· Make recommendations to the Council on financial, internal control and risk management policy and procedure matters as appropriate.

· To approve the Auditors’ engagement and arrangements letters in relationship to the Annual Report.

|

Audit and Risk Committee Meeting Agenda |

27 February 2020 |

Notice is hereby given that a Audit and Risk Committee

Meeting will be held in the Council

Chambers, Barkes Corner, Tauranga on:

Thursday, 27 February 2020 at 1.00pm

9.1 Work Programme for Audit and Risk Committee.

9.2 Annual Audit and LTP Monitoring Reports

9.3 Three Year Internal Audit Plan (KPMG)

9.5 Annual Plan Assumptions Update

1 Present

|

27 February 2020 |

9.1 Work Programme for Audit and Risk Committee

File Number: A3685429

Author: Kumaren Perumal, Group Manager Finance and Technology Services

Authoriser: Kumaren Perumal, Group Manager Finance and Technology Services

Executive Summary

1. Council agreed to establish an Audit and Risk Committee at its 7 November 2019 meeting. The purpose of this report is to seek approval of a Work Programme for the Committee for 2020.

|

1. That the Group Manager Finance and Technology Services report dated 17 February 2020 and titled ‘Work programme for Audit and Risk Committee’ be received. 2. That the Audit and Risk Committee 2020 Work Plan (Draft) be approved. |

Background

2. Council agreed the establishment of an Audit and Risk Committee at its 7 November 2019 meeting with Mayor Webber appointed as Chairperson and Councillor Denyer appointed as Deputy Chairperson.

3. In recent years the Office of the Auditor General and Local Government New Zealand have strongly advocated for the creation of Audit and Risk Committees in the local government sector. Several neighbouring Councils have already established these committees and they are widely seen as good practice. Across the country around two-thirds of Council’s have Audit and Risk Committees.

4. The role of the Audit and Risk Committee is to provide assurance and assistance to Council on the management of Council’s risk, financial control and compliance framework and its external accountability responsibilities. The Terms of Reference, as approved by Council at its 5 December 2019 meeting.

Scope of Committee

5. The scope of the Committee focuses on risk management, financial control, compliance and external accountability. It includes development and monitoring of an appropriate risk management strategy, internal and external audit arrangements, the oversight and development of Council’s Annual Report, financial and corporate policies and improvements to management, performance and internal controls. It will provide a dedicated and regular forum at the governance level for Council’s relationship with its audit service provider.

Work Programme

6. A draft work programme outlining discussion topics for each meeting in 2020 is attached for the Committee’s approval (Attachment 1).

Monitoring and Reporting

7. At each meeting of the Audit and Risk Committee, a report will be considered providing a status update on outstanding audit management report items (internal and external) arising from previously received audit management reports.

Independent oversight

8. Following a formal procurement process, an external consultant will be appointed to undertake an independent review of the performance and effectiveness of the Audit and Risk Committee on an annual basis. The results of this review will be reported to the Committee at its November meeting

1. 2020

Committee Workplan (Draft) ⇩ ![]()

|

1. Audit and Risk Committee Meeting Agenda |

2. 27 February 2020 |

|

Workstream |

Committee meeting date

|

||||||

|

|

Feb 2020 |

May 2020 |

Aug 2020 |

Nov 2020

|

|||

|

Work Plan |

|||||||

|

Agree Audit and Risk Committee 2020 Workplan

|

√ |

|

|

|

|||

|

Risk Management |

|||||||

|

Quarterly review of Risk Profile |

|

|

√ |

√ |

|||

|

Annual Refresh of Risk Profile (Top-down strategic risk identification & assessment – our top 12 risks. |

|

√ |

|

|

|||

|

Internal Audit (KPMG) |

|||||||

|

Three Year Internal Audit Plan |

√ |

|

|

|

|||

|

2019/20 Internal Audit area of focus |

|

√ |

|

|

|||

|

Internal Audit Reporting / Monitoring |

|

√ |

√ |

√ |

|||

|

Policy / Strategy Input |

|||||||

|

Review and input into various policies and strategies such as the Sensitive Expenditure Policy, Fraud Policy as relevant.

|

|

√ |

√ |

√ |

|||

|

Insurance / Treasury / Tax |

|||||||

|

Insurance Renewal Process Summary |

|

|

√ |

|

|||

|

Treasury Update |

√ |

√ |

√ |

√

|

|||

|

Tax Governance Framework |

|

|

√ |

|

|||

|

External Audit and External Accountability |

|||||||

|

Annual Plan Assumptions / Update

|

√ |

|

|

|

|||

|

Audit Arrangements Letter 2019/20 |

|

√ |

|

|

|||

|

Review of Accounting Policies, Key Accounting Estimates and Update on Asset Revaluation Results |

|

√ |

|

|

|||

|

Approval of Draft Annual Report 2019/20 |

|

|

√ |

|

|||

|

Interim Audit Management Report 2019/20 |

|

√ |

|

|

|||

|

Final Audit Management Report 2019/20 |

|

|

|

√

|

|||

|

Audit Management Report 2018/19 |

√ |

|

|

|

|||

|

LTP Audit Management Report 2018/28 |

√ |

|

|

|

|||

|

Audit Management Monitoring Report [LTP and Annual Audit]

|

√ |

√ |

√ |

√ |

|||

|

Other |

|||||||

|

Procurement Governance Framework / Policy Review |

|

√ |

|

|

|||

|

Independent review of performance and effectiveness of the audit and Risk Committee. |

|

|

|

√ |

|||

|

27 February 2020 |

9.2 Annual Audit and LTP Monitoring Reports

File Number: A3685487

Author: Ian Butler, Finance Manager

Authoriser: Kumaren Perumal, Group Manager Finance and Technology Services

Executive Summary

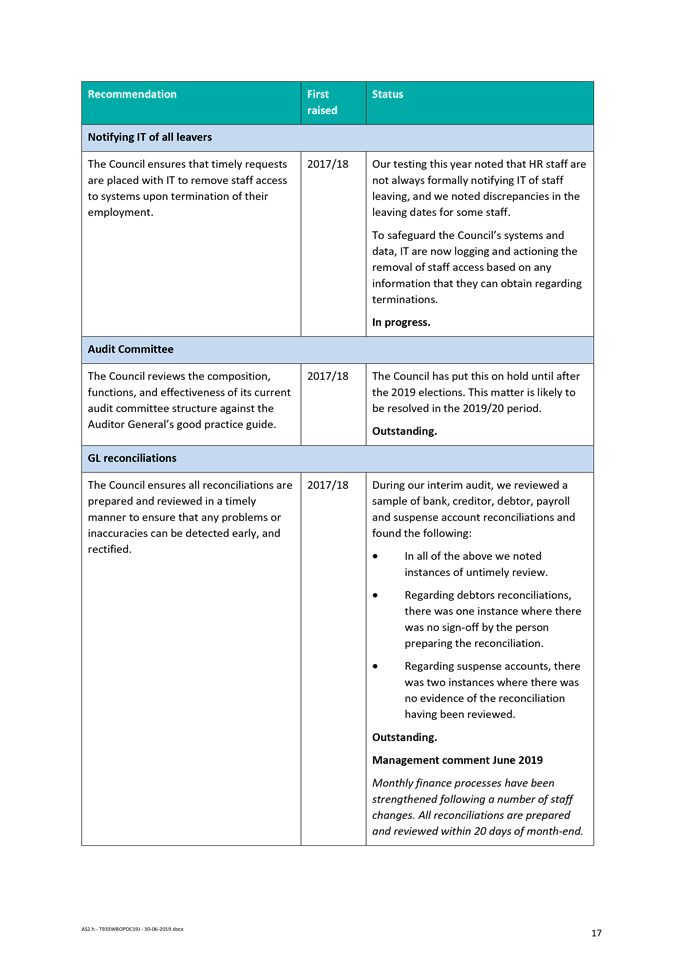

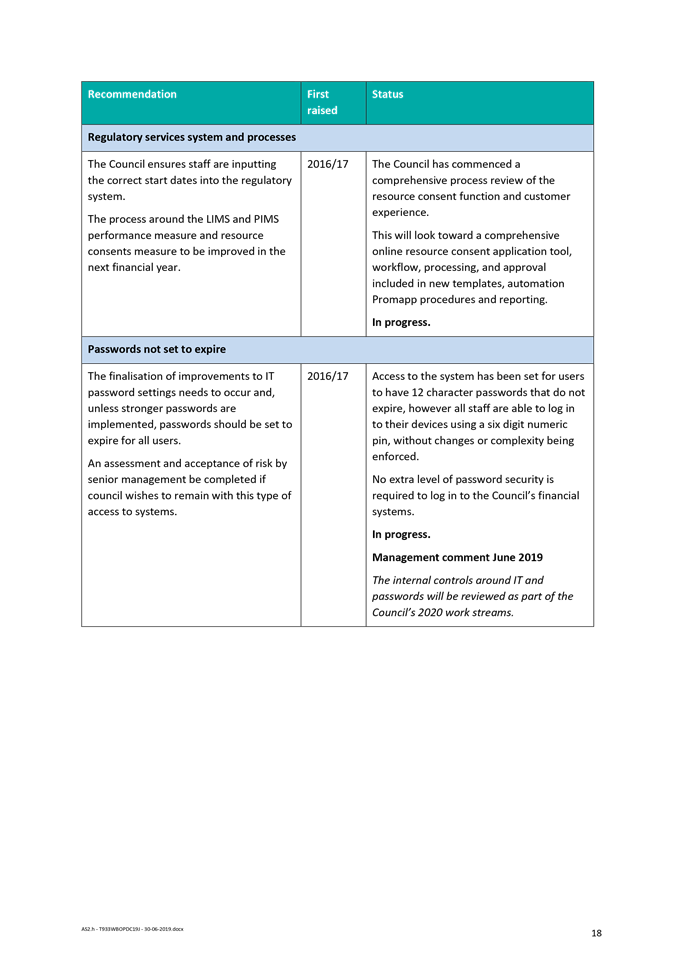

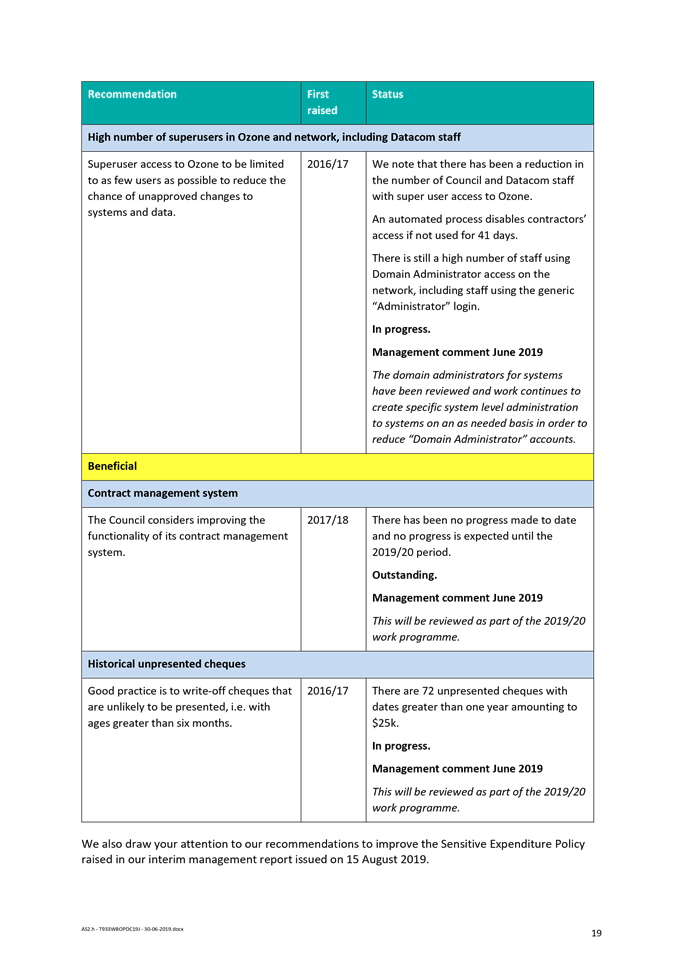

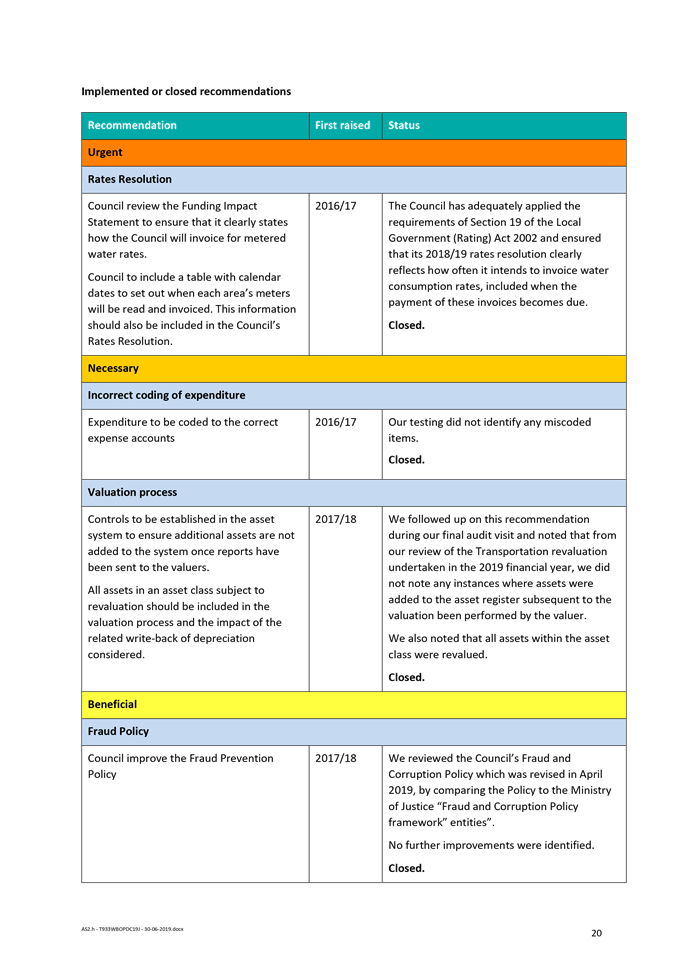

1. This report provides an overview of the issues raised by Audit New Zealand in their management reports for the audits carried out for the 2018-28 Long Term Plan (Attachment 1) and the 2018/19 Annual Report (Attachment 2). This report also provides management responses to those issues identified and an update of progress made against those issues.

2. A monitoring report will be presented at each Committee meeting setting out the latest progress on management‘s response to each issue.

|

That the Finance Manager and Senior Financial Planner‘s report dated 14 February 2020 and titled ‘Annual Audit and LTP Monitoring Reports’ be received. |

Background

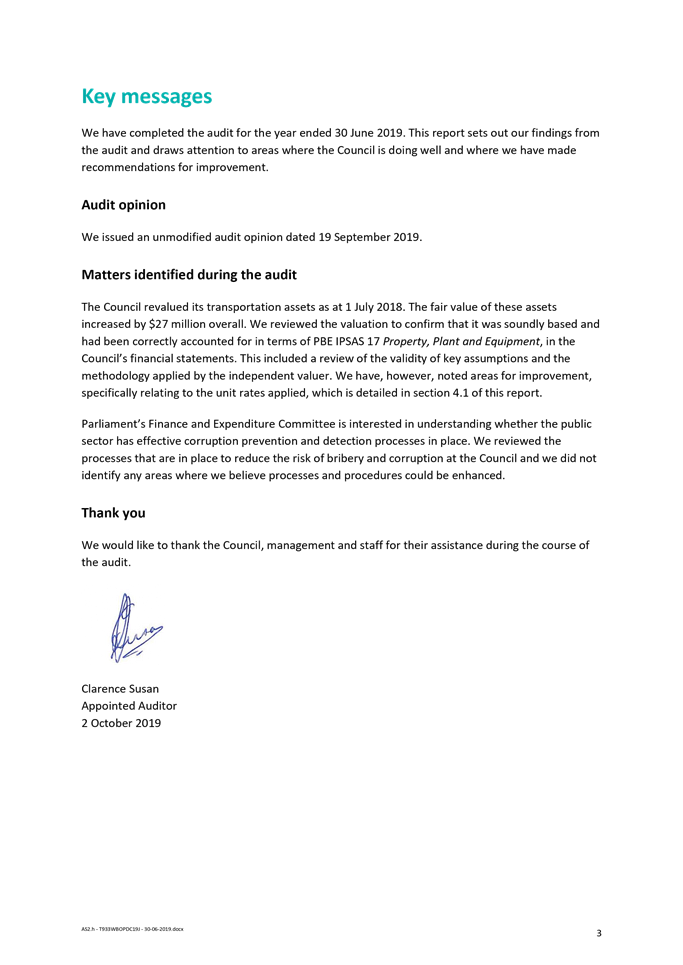

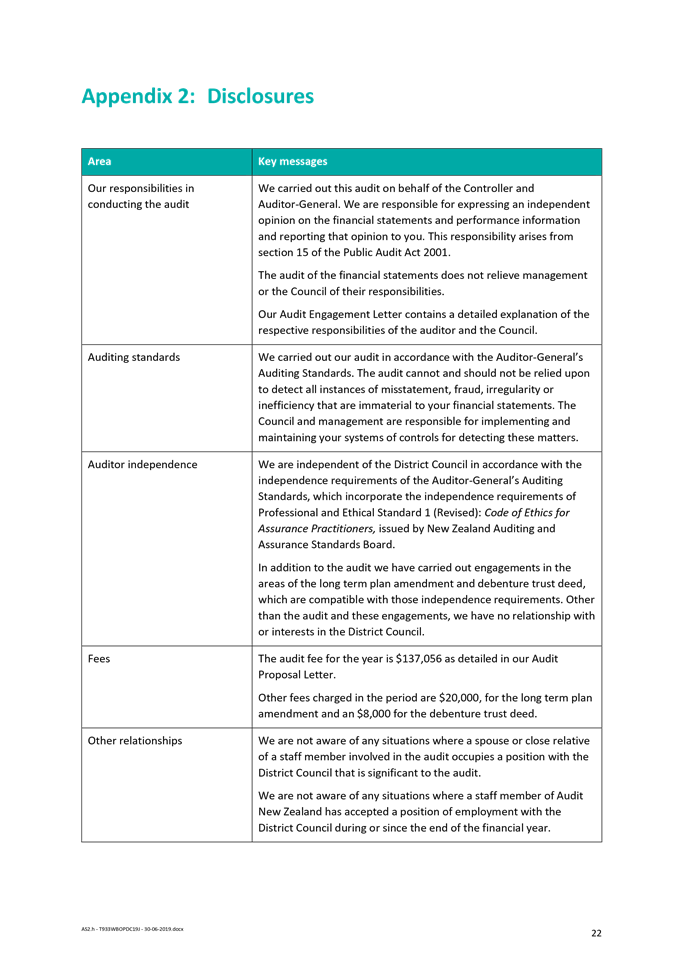

3. The Local Government Act 2002 requires Local Authorities to have their Annual Reports and Long-Term Plans audited by the Auditor-General. The Auditor-General has appointed Audit New Zealand as Council’s audit service provider.

4. This process of auditing the Annual Report and Long-Term Plan involves Audit New Zealand issuing an opinion that the information published in these documents fairly present the Council’s financial position and comply with legislation.

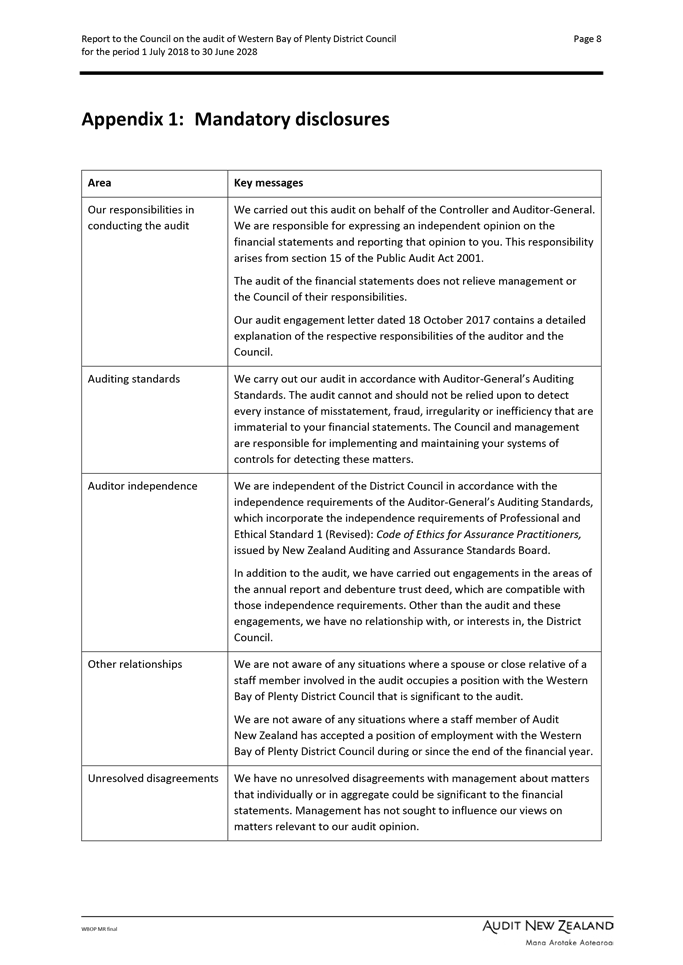

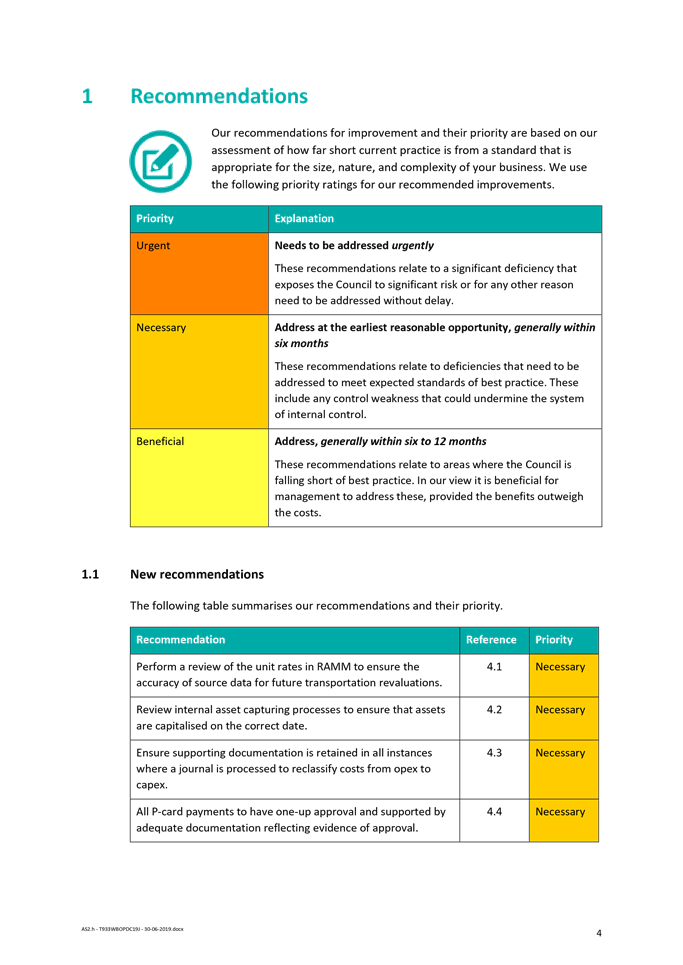

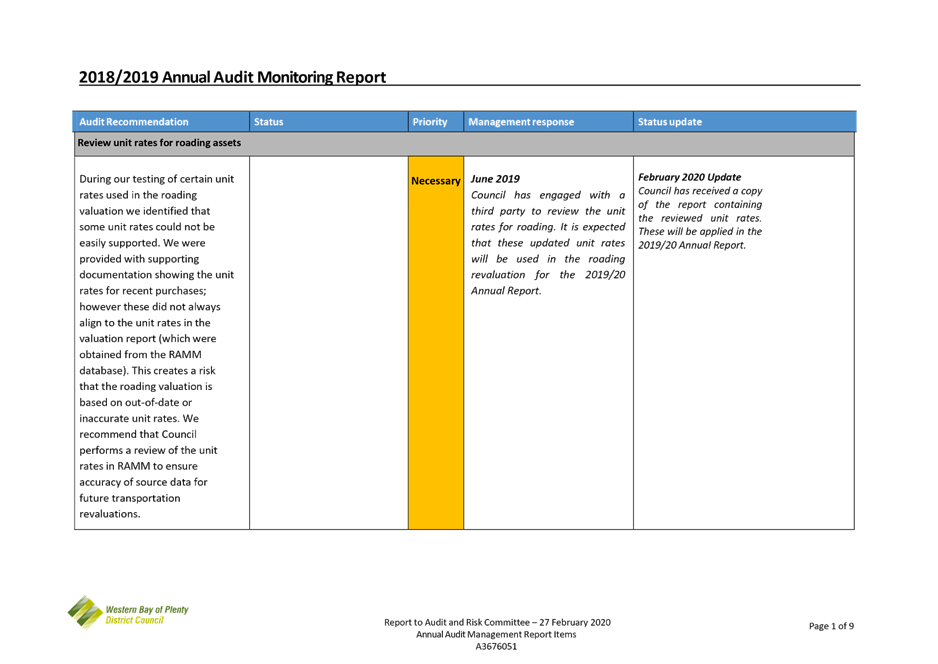

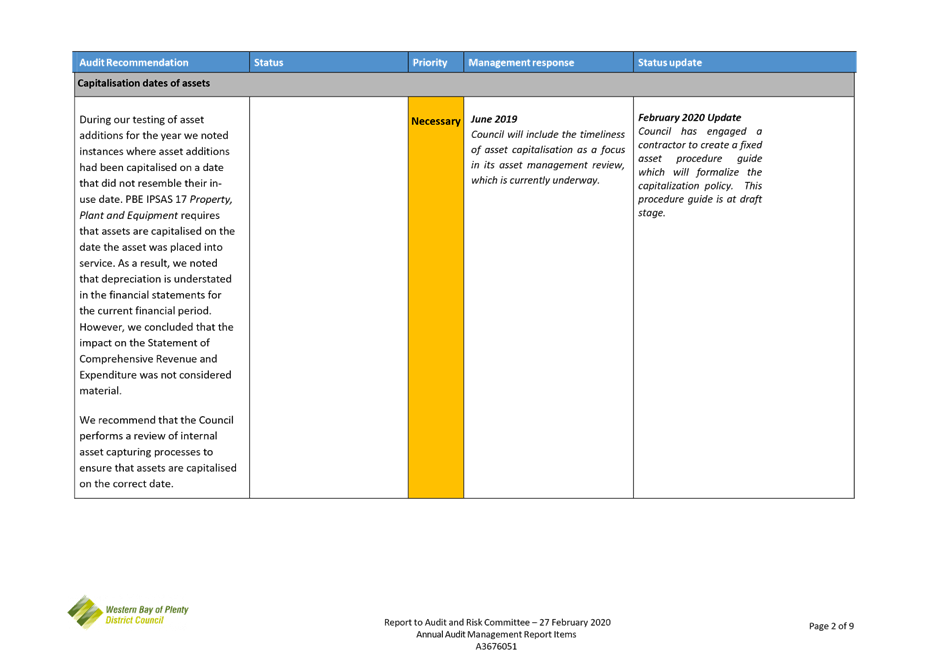

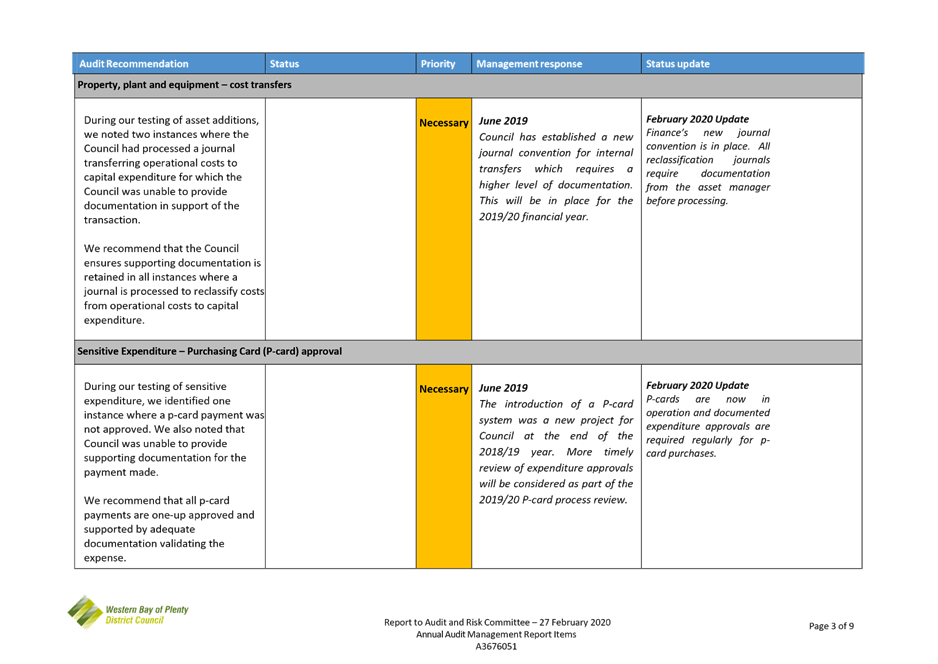

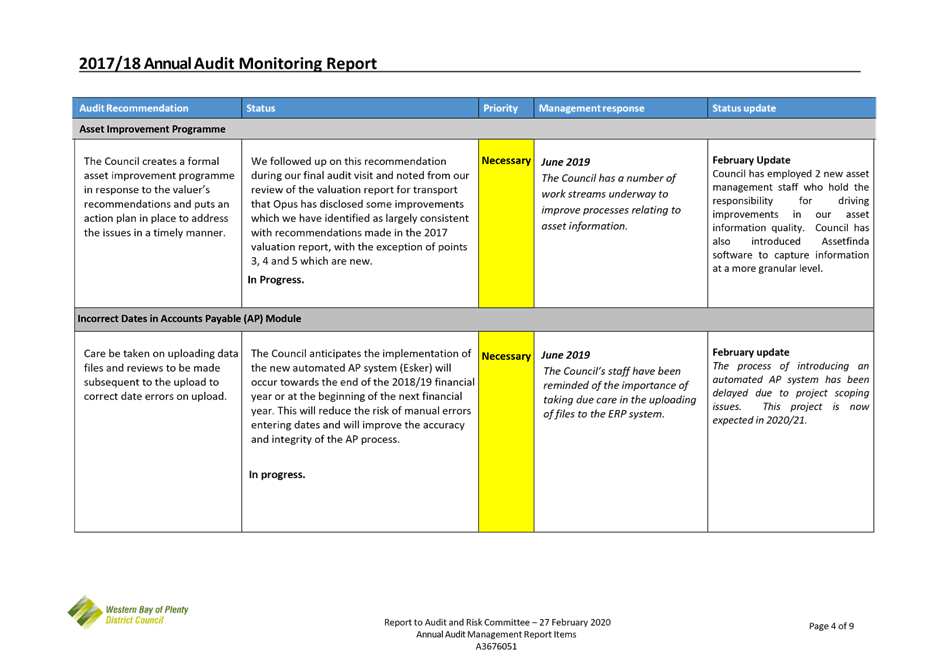

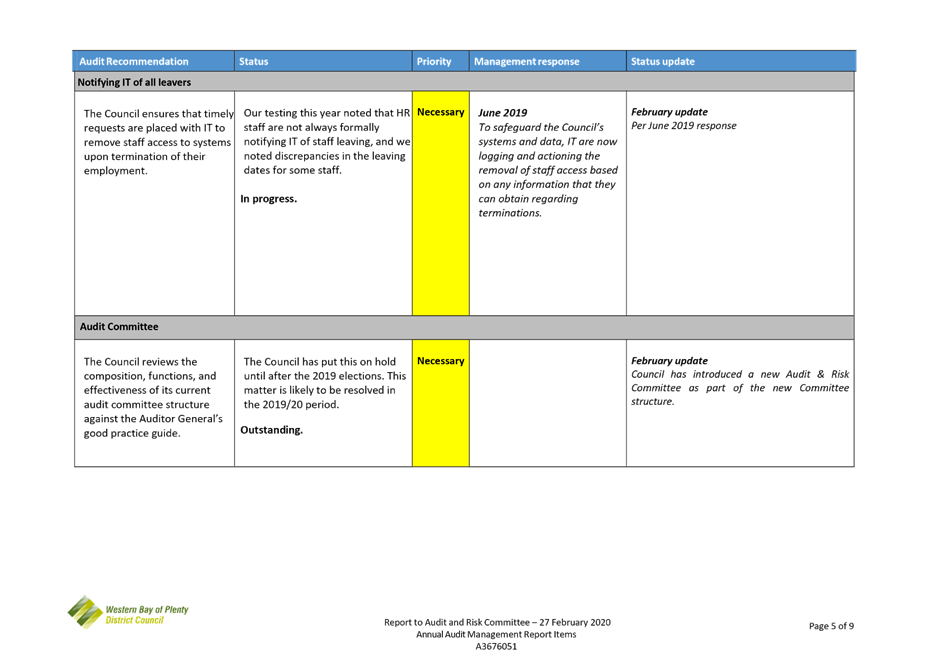

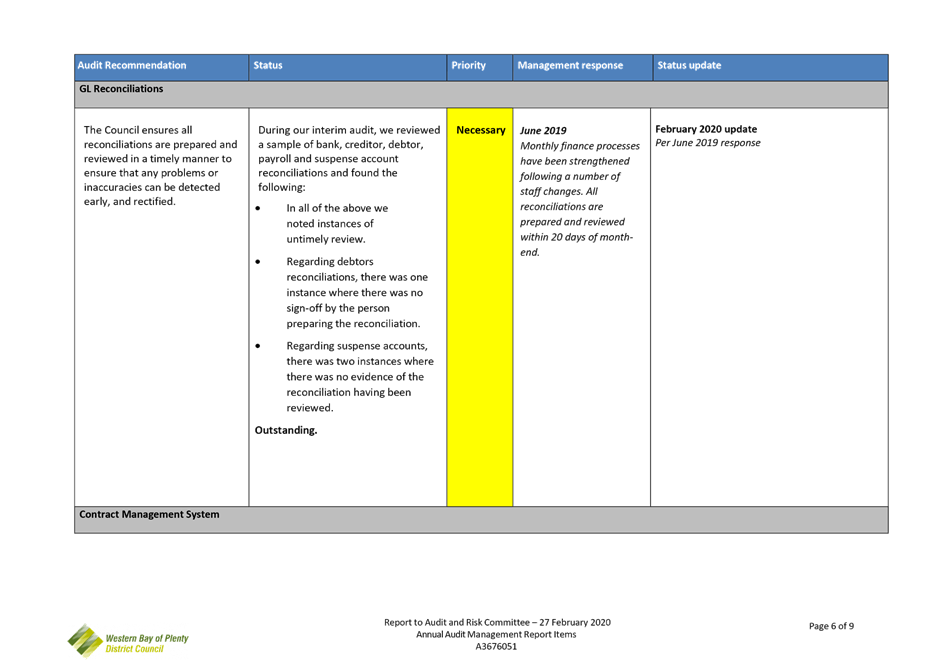

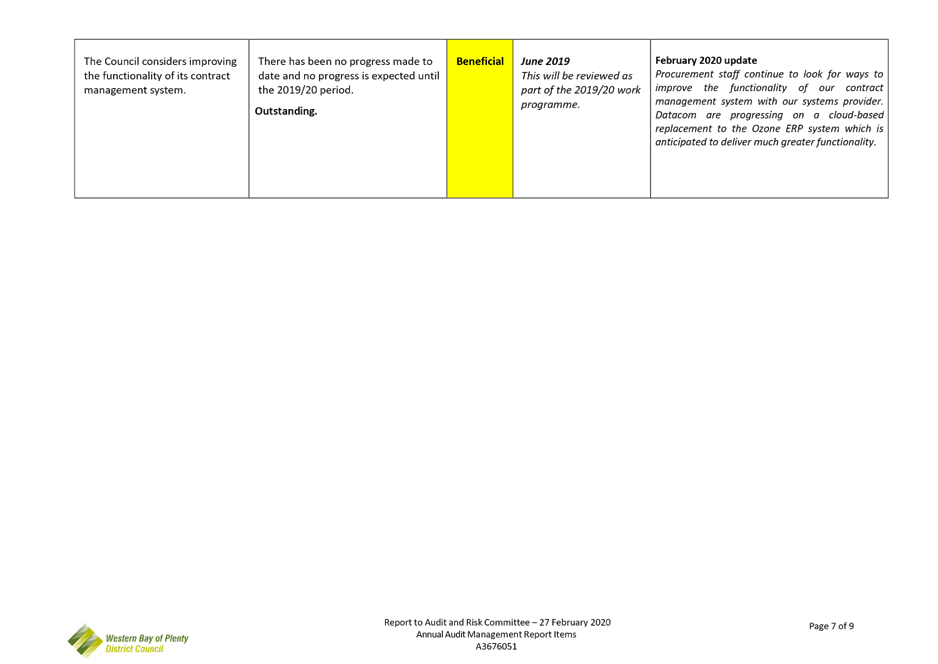

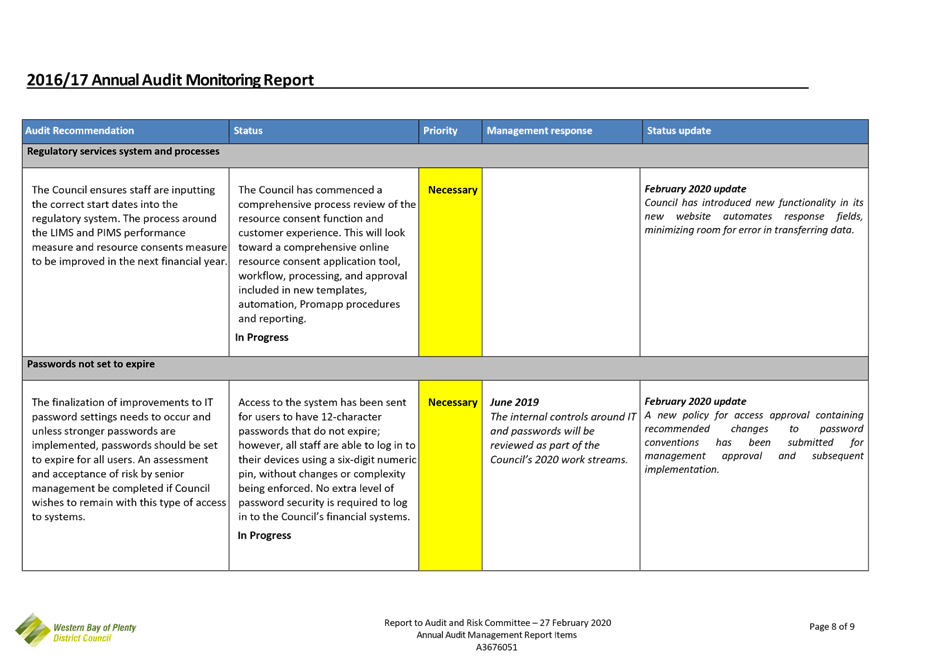

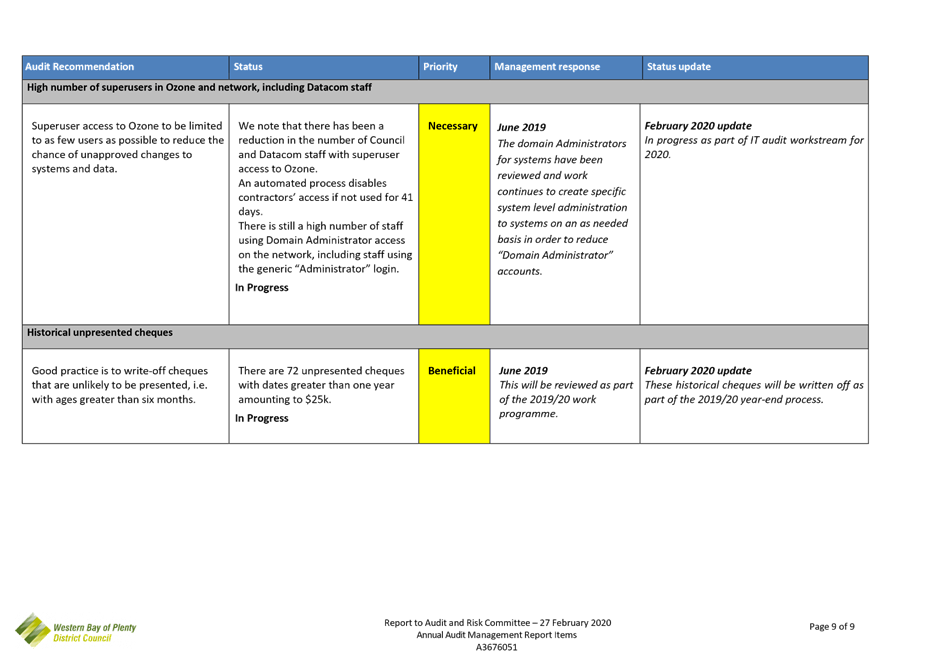

5. At the conclusion of each audit, Audit New Zealand provide a management report highlighting any issues they find, the degree of severity of the issue and a recommendation. Issues raised by Audit New Zealand are classed as “Urgent, Necessary or Beneficial“.

6. This report provides an overview of the issues raised by Audit New Zealand during their audits of both the 2018-28 Long Term Plan and the 2018/19 Annual Report. This report also provides management responses to those issues identified and an update of progress made against those issues.

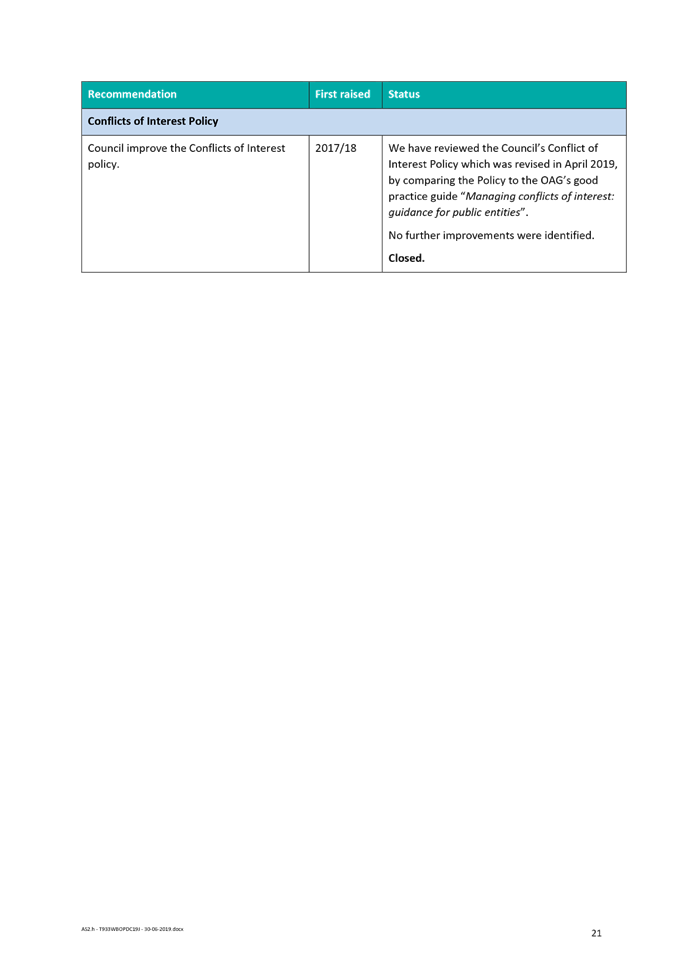

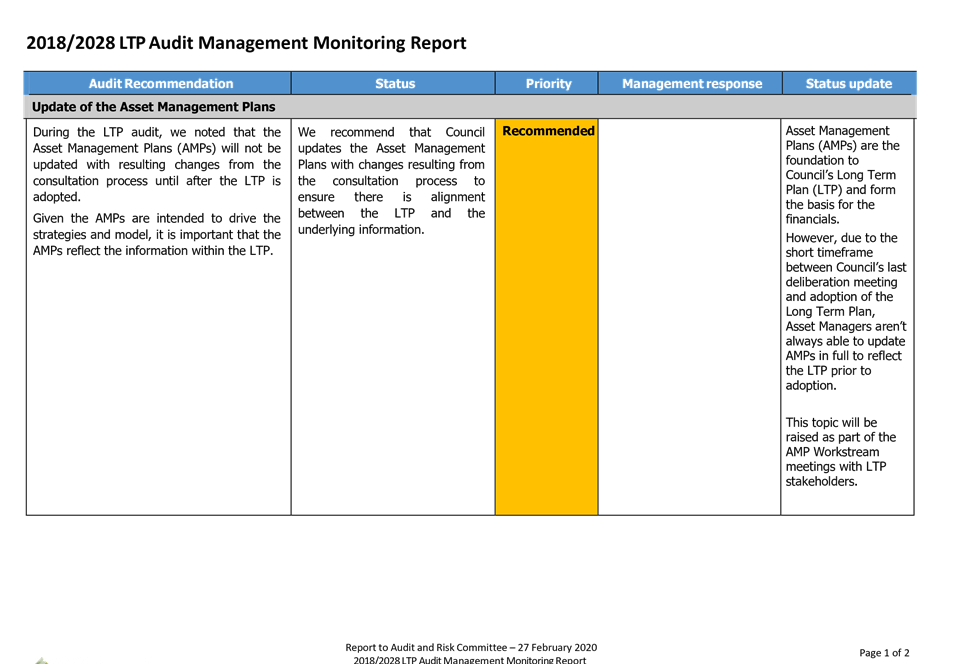

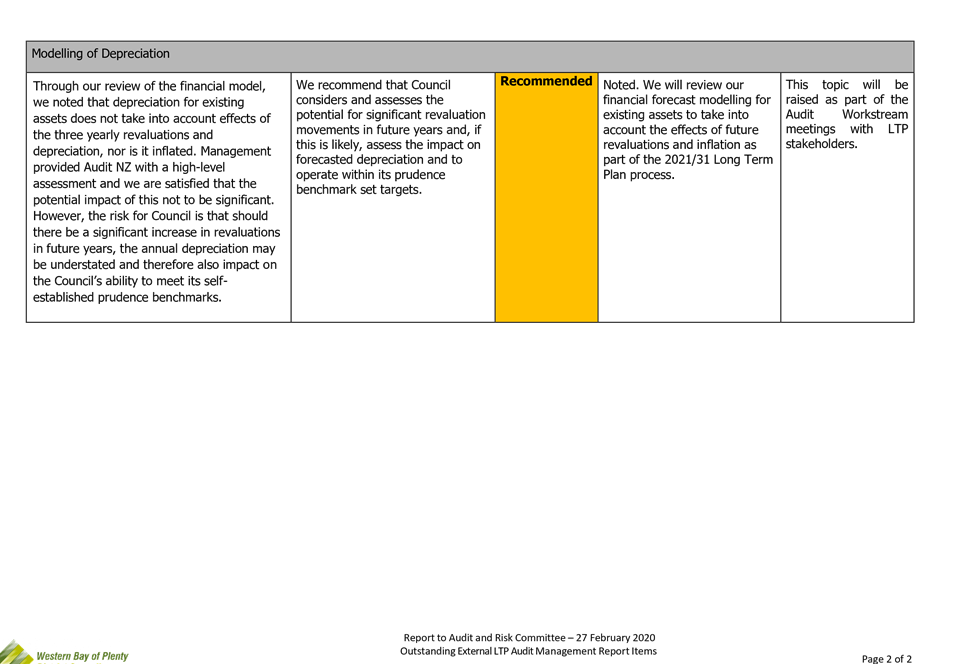

Management report - 2018-28 Long term plan

7. The Management Report on the 2018-28 Long Term Plan identified 2 prior issues (classed as recommended) carried over from the 2018-28 Long Term Plan. These two issues and their status updates are outlined in Attachment 3.

management report – 2018/19 annual report

8. The Management Report on the Annual Report 2018/19 identified 10 prior issues (8 classed as necessary, 2 classed as beneficial) carried over from the Annual Report 2017/18 where Council is in various stages of implementation. These issues and their status updates are outlined in Attachment 4.

9. The report identified 4 new issues (all classed as necessary) relating to the 2018/19 Annual Report. These issues and their status updates are outlined in Attachment 4.

10. The report also identified 5 prior issues that where able to be closed as Council had implemented the process change recommended by Audit New Zealand.

1. Audit

NZ - LTP Audit Report 2018-2028 ⇩ ![]()

2. Audit

NZ Report to the Council - Audit of the year ended 30 June 2019 ⇩ ![]()

3. 2020

LTP Audit Monitoring Table (Audit NZ) ⇩ ![]()

4. 2020

Annual Audit Monitoring Table (Audit NZ) ⇩ ![]()

|

27 February 2020 |

9.3 Three Year Internal Audit Plan (KPMG)

File Number: A3685496

Author: Kumaren Perumal, Group Manager Finance and Technology Services

Authoriser: Kumaren Perumal, Group Manager Finance and Technology Services

Executive Summary

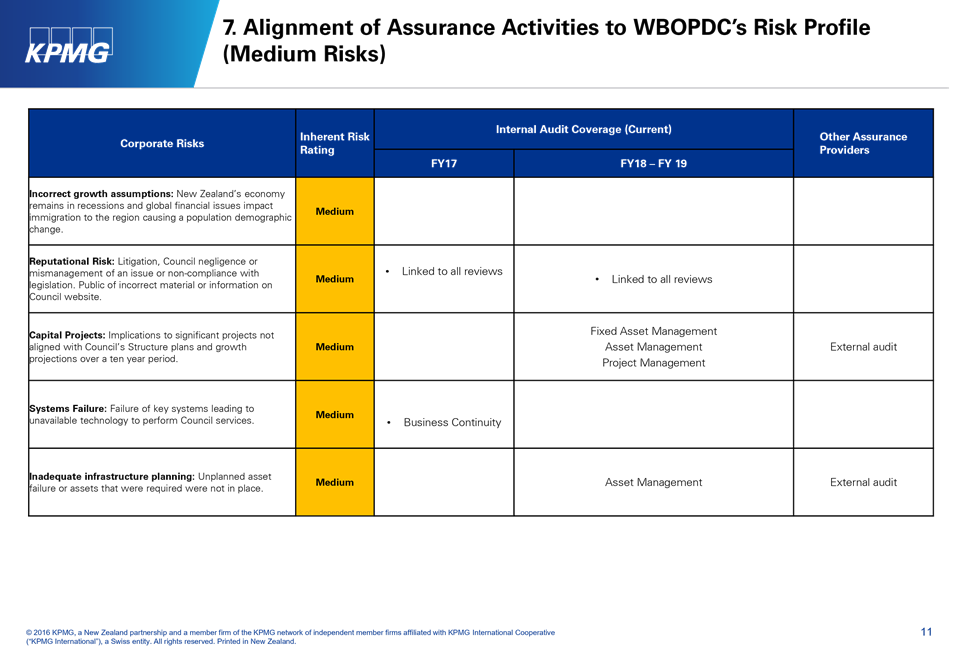

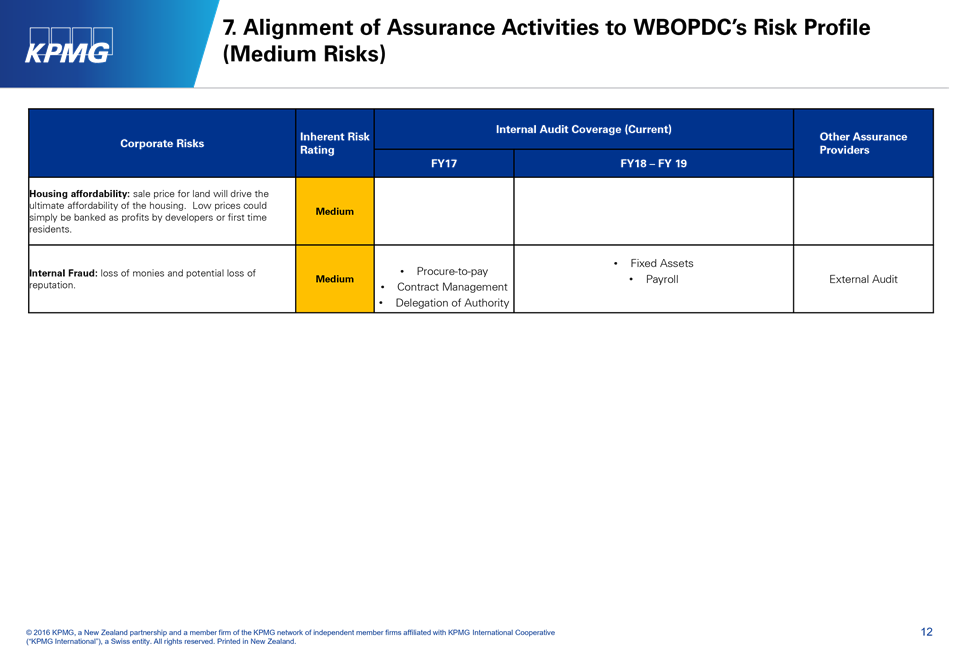

1. The purpose of this report is to provide the Audit and Risk Committee with an overview of Council’s three-year internal Audit Plan for the 2017, 2018 and 2019 financial years.

|

2. That the Group Manager Finance and Technology’s report dated 17 February 2020 and titled “Three Year Internal Audit Plan” be received. 3. That the report relates to an issue that is considered to be of low significance in terms of Council’s Significance and Engagement Policy. |

Background

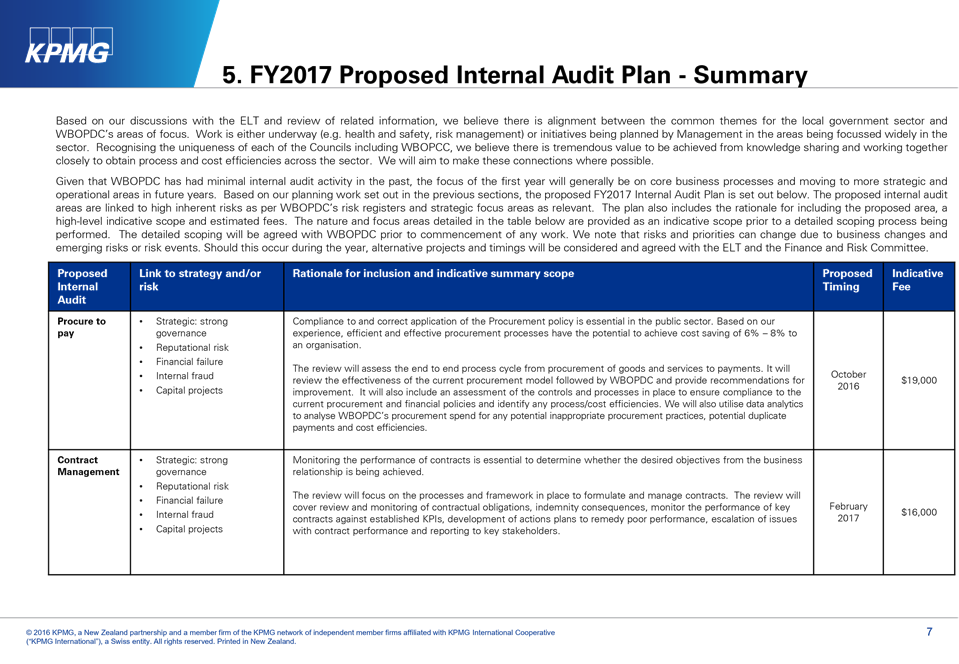

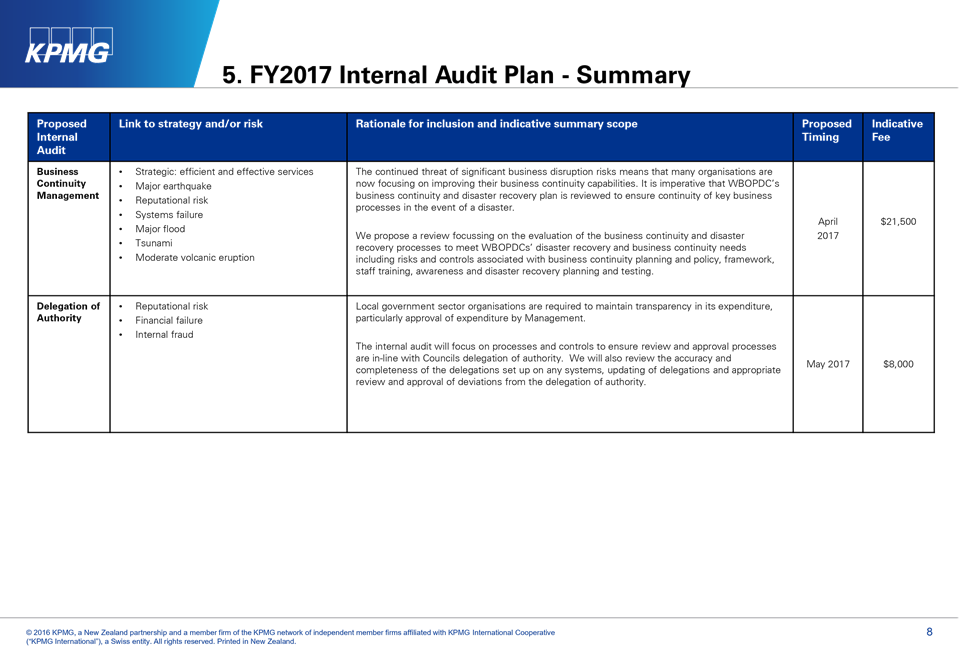

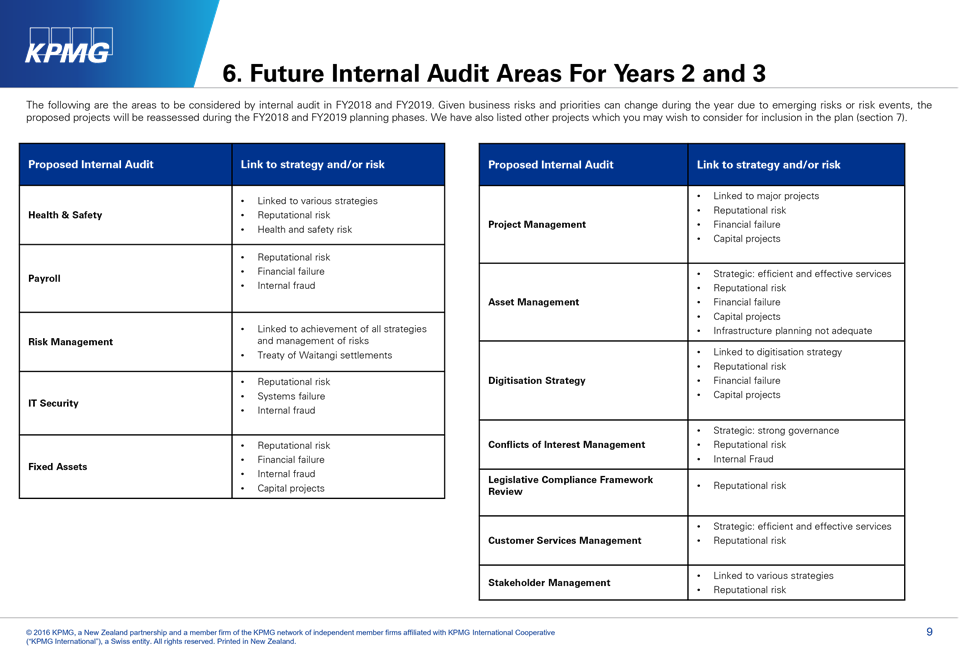

4. During the 2016/17 financial year KPMG was appointed as Council’s Internal Auditor under a BOPLASS arrangement and worked with Council staff to establish a three-year internal audit plan (Attachment 1).

5. The Audit Plan outlines the intended areas of focus for 2017, 2018 and 2019 with confirmation sought from senior management on an annual basis.

6. Areas that were reviewed during the 2017-2019 audit period and agreed between audit and management include:

|

2017 |

Procurement |

|

2017 |

Contract Management |

|

2018 |

Risk Management |

|

2018 |

Asset Management |

|

2018 |

Financial Controls Review |

|

2019 |

Project Management |

The only workstream not covered in the 2017-2019 Audit Plan was the Financial Controls Review. As Council were already in the process of reviewing Business Continuity Management and Delegations of Authority, it was agreed KPMG would not progress these areas of focus.

7. A monitoring report setting out the findings for the various areas of Council’s operations that were reviewed under this plan will be reported at the May Audit and Risk Committee meeting. This report will also include management’s response to these findings along with its current status.

1. 3

Year KPMG Internal Audit Plan Final ⇩ ![]()

|

27 February 2020 |

File Number: A3684279

Author: David Jensen, Senior Financial Planner

Authoriser: Kumaren Perumal, Group Manager Finance and Technology Services

Executive Summary

1. This report provides an overview of the risks associated with Council’s treasury function and the procedures in place to mitigate those risks.

|

That the Senior Financial Planners report dated 14 February 2020 and titled ‘Treasury Update’ be received. |

Executive Summary

2. Council identifies, monitors and reports on risks related to its treasury function through the Performance and Monitoring Committee. Council also engages Price Waterhouse Coopers (‘PwC’) as advisors on treasury matters and meet on a monthly basis to discuss Council’s position.

3. Based on Council’s low inherent risk as a Local Authority, its regular monitoring and reporting, the review by PwC and the clear rules set under the Treasury Policy, Council’s treasury function is viewed as being low risk.

Background

4. Council has a treasury function which manages Council cash, investments and debt. This function is performed in accordance with Council’s Treasury Policy, which sets the framework for staff responsibilities and delegated authorities, policies for debt and investments and the process for managing risks associated with the treasury function.

5. Council also engage Price Waterhouse Coopers (“PwC”) as advisors on treasury matters. PwC review Council’s treasury positions on a month basis and meet on a monthly basis to discuss markets events, Council forecasts based on Annual Plans/Long Term Plans and how Council should position itself in accordance with best practice.

6. Council’s Treasury Policy is designed to identify and manage risks, which are discussed further below.

Intrest rate risk

7. Interest rate risk is the risk that either investment returns will fall materially short of forecast, or that financing costs will exceed projections due to adverse movements in interest rates.

8. Council has a policy which establishes rules for how much of Council’s debt should be fixed rate vs variable interest rate, looking forward for 16 years. This ensures that Council is not exposed to volatile movements in the interest rate market.

9. These rules are reviewed by PwC every 3 years as part of the Treasury Policy review.

10. Council then uses these rules to engage in hedging with major trading banks, minimising Council’s exposure to volatile changes in interest rates.

11. As a result of the rules provided by the treasury policy and the support provided by third party advisory, Council has a low level of interest rate risk.

Liquidity and Funding Risk

12. Liquidity risk is the risk that Council may not have enough liquid cash or committed facilities on hand to fund operations. This is due to the fact that Council’s cash flow is dependent on the maturity of cash investments and loans.

13. Funding risk focuses on Council’s ability to refinance old loans or raise new loans at the time required with favourable pricing.

14. Council has a policy which sets how much debt can be borrowed short term or long term and identifies how loans should be structured to ensure that loan maturities are spread over time, not lumped together. This ensures that whenever Council refinances or pays a maturity it can be easily cash flowed.

15. Council also has a committed facility with ANZ Bank for $30 Million. This has never been drawn down on.

16. As a result of the rules provided by the treasury policy for debt maturity and the existence of committed bank lines, Council has a low level of liquidity and funding risk.

Foreign Exchange risk

17. Foreign exchange risk is the risk that volatile movements in foreign currency may adversely affect the cost to Council of entering into arrangements with offshore parties.

18. Council has minor foreign exchange risk through the occasional purchase of overseas denominated services, plant and equipment.

19. Council has a policy which establishes rules for how large a contract may be entered into without using hedge contracts.

20. Under this policy, Council is forbidden from borrowing money or holding investments denominated in foreign currency.

21. As a result of the rules provided by the treasury policy for foreign currency purchases and the low degree to which it occurs, Council has a low level of foreign exchange risk.

Counterparty Credit risk

22. Counterparty credit risk is the risk of losses occurring as a result of a counterparty default.

23. Council has a policy which establishes rules for the maximum value of investments or hedging contracts that can be entered into with any one party. There are also minimum credit rate requirements, placing a floor under a credit rating of A as approved by rating agencies Standard & Poors or Fitch.

24. As a result of the rules provided by the treasury policy for counterparties, Council has a low level of counterparty credit risk.

|

27 February 2020 |

9.5 Annual Plan Assumptions Update

File Number: A3684383

Author: David Jensen, Senior Financial Planner

Authoriser: Kumaren Perumal, Group Manager Finance and Technology Services

Executive Summary

1. This report provides an update on the assumptions accepted by Council for the 2020/21 Annual Plan during the Annual Plan Workshop on the 3rd December 2019 and whether any risks exist for these assumptions.

2. The risk that market conditions will change materially in the short term, altering assumptions for the 2020/21 Annual Plan is low.

Background

3. During the Annual Plan Workshop on the 3rd December 2019 Elected Members accepted the underlying assumptions for interest rates, inflation and growth into the Annual Plan 2020/21.

4. Staff continue to test these assumptions against actual market movement in order to gain comfort that the assumptions included in the 2020/21 Annual Plan match the likely operating environment for that year.

Interest Rates

5. Council adopted the 2018-28 Long Term Plan on 28 June 2018. This held an interest rate assumption of 6%, which was to be re-tested annually through the Annual Plan process.

6. During the Annual Plan Workshop on 3 December 2019, staff recommended to Elected Members that the 6% interest rate assumption should be reduced to 4.5% based on market movement and Council’s actual cost of borrowings had decreased significantly from the adoption of the 2018-28 Long Term Plan.

7. Elected Members accepted an assumption of 4.5% and this was incorporated into draft budgets for the 2020/21 Annual Plan.

8. Since 3 December 2019 market interest rates have maintained their low trajectory. The Reserve Bank kept the Official Cash Rate at 1% during the February Monetary Policy Statement, with no rate increases priced in for the remainder of the 2020 calendar year.

9. As interest rates are forecast to hold lower for the foreseeable future, the risk to Council’s interest rate assumption for the 2020/21 Annual Plan is low.

Inflation

10. Council adopted the 2018-28 Long Term Plan on 28 June 2018. This held an inflation rate assumption of 2.20% for the 2020/21 financial year.

11. Council uses the Local Government Cost Index (‘LGCI’) to measure inflation along with most councils in New Zealand, which is produced by Business and Economic Research Limited (‘BERL’).

12. BERL produced an updated version of the LGCI during 2019. Their report noted that while the cost of running certain Council activities had either increased or decreased, as an average the original 2.20% assumption was still valid for the 2020/21 financial year.

13. During the Annual Plan Workshop on 3 December 2019, staff recommended to Elected Members that the inflation rate assumption of 2.20% should be maintained.

14. Elected Members accepted the inflation rate assumption of 2.20% and this was retained in the draft budget.

15. As Council’s inflation rate assumption has been prepared and re-tested by an independent expert with a long record of accuracy in predicting cost escalations for Local Authorities, the risk to Council’s inflation rate assumption for the 2020/21 Annual Plan is low.

Growth

16. Council adopted the 2018-28 Long Term Plan on 28 June 2018. This held a growth assumption for additional rating units of 1.28% for the 2020/21 financial year.

17. Growth assumptions for the 2018-28 Long Term Plan were assessed using projections made by Smartgrowth, a strategic partnership between Western Bay of Plenty District Council, Tauranga City Council, Bay of Plenty Regional Council, tangata whenua, and business agencies.

18. The results of the 2018 New Zealand Census were compared to the 2018-28 LTP projection which showed that while the Western Bay’s population had grown significantly more than forecast, the growth in the number of rating units was fairly close to forecast. This update matched the changes in the Western Bay’s demographics, with more people living in one dwelling than before.

19. In assessing the likely level of growth in rating units for the 2020/21 Annual Plan, Council took a conservative lens in order not to overstate the district’s likely growth.

20. During the Annual Plan Workshop on the 3 December 2019, staff recommended to Elected Members that the growth rate assumption for new dwellings should be increased from 1.28% to 1.38%.

21. Elected Members accepted the growth assumption of 1.38% and this was included in the draft budget.

22. As Council’s growth rate assumption has been informed by actual district growth identified through the Census and calculated through a conservative lens, the risk to Council’s growth rate assumption for the 2020/21 Annual Plan is low.